Posted by PrimeTrust Advisors | March 9, 2023

401(k)s – How Much to Contribute? (Video)

By Chip Hunt

When it comes to saving for retirement, there’s no better savings vehicle than a trusty 401(k). But it must be used properly for maximum benefit. One of the single biggest 401(k) mistakes I see is many workers only contribute enough to get the full company matching amount. And that’s it; they stop there.

For example, if the company’s matching formula is 50% of what you put in, up to 6% of pay, most folks aim for that 6% rate. And somehow that amount is often mistakenly assumed to be the correct savings rate. In most cases, that is absolutely not true at all! Below, I’ll show you why.

In this tutorial article, my purpose is to give you a better understanding of how much you need to contribute, as well as, how much money you should already have saved by now. Let’s jump in.

The Question

Everyone wants to know, “How much should I contribute to my 401(k) plan?” First, we must discuss the primary factor influencing that decision: what is your goal? Knowing what your goal is essentially leads you to the answer of how much you will need to contribute. Let’s discuss how to think about what your goal is, and then how to figure out how much you should be contributing to meet that goal.

Set Your Goal

One way to think about setting your goal is to understand that you are trying to create a pension for yourself. Thirty to forty years ago most people had a company pension and Social Security to provide a regular stream of paychecks to live on in retirement. As you know, pensions are mostly gone and 401(k) savings plans have taken their place, leaving you as the chief decision-maker. Now you must fill in the gap—you have to create your own pension.

You must decide how much to contribute, how to invest, and eventually how to withdraw the money so you can provide yourself a regular stream of paychecks to live on in retirement. It’s no small task. And that’s why it’s helpful to know a pension guy who may be able to help you.

In retirement you’re going to need a regular paycheck for as long as you live. And that paycheck needs to be reasonably close to what you were making while you were working. So thinking about it this way, your retirement goal can be stated as the need to receive a paycheck equal to some percentage of what you were making before retirement. But what percentage should you use? Of course, everybody’s going to be a little different, but here’s a good starting place.

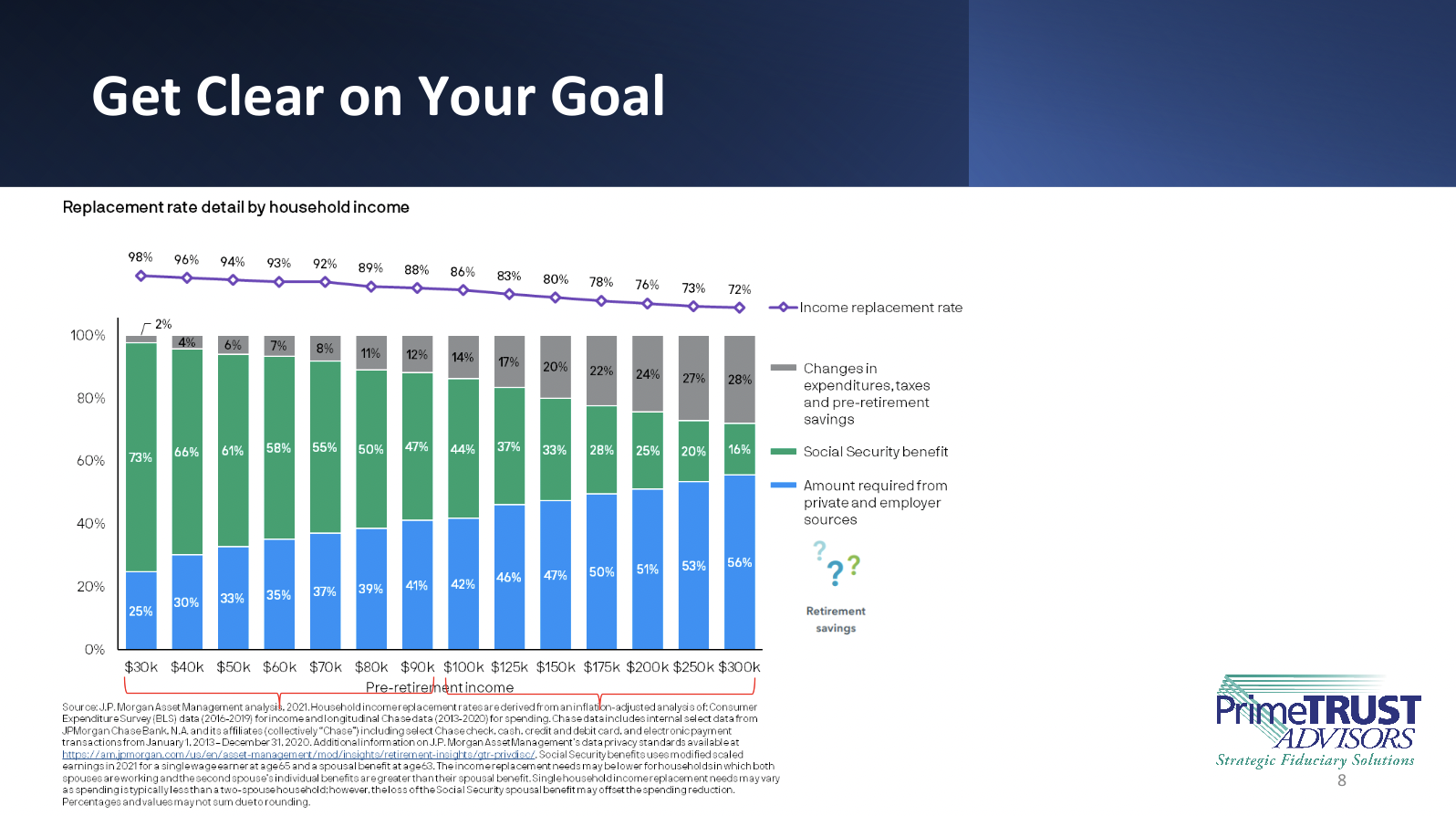

Based upon research provided by J.P. Morgan, this chart provides a guide to help you in setting a retirement goal. (It looks complex, but it’s actually very simple.) Here you can see suggested percentage amounts (across the top) at various levels of pre-retirement household income (shown across the bottom). For example, someone with a combined household income of $50,000 would likely need paychecks equal to 94% of what they were making before retirement. And if 94% is the retirement goal, and Social Security income (shown in green) provides 61% of that, then the specific goal for the retirement plan (meaning the 401(k) plan) is to fill that gap; that is to provide regular paychecks of 33% of your pre-retirement income.

So, in this example, we just accomplished the first step of identifying your goal. Hit the 33% mark! Now, as we said at the start, understanding that goal leads you to ask, “How much should I be contributing to meet my goal?” Well, the answer to that question depends upon three things: your age, how much you currently make, as well as, how much you have already saved.

How Much to Contribute?

Considering the factors of age and income, here are suggested contribution guidelines for funding your goal:

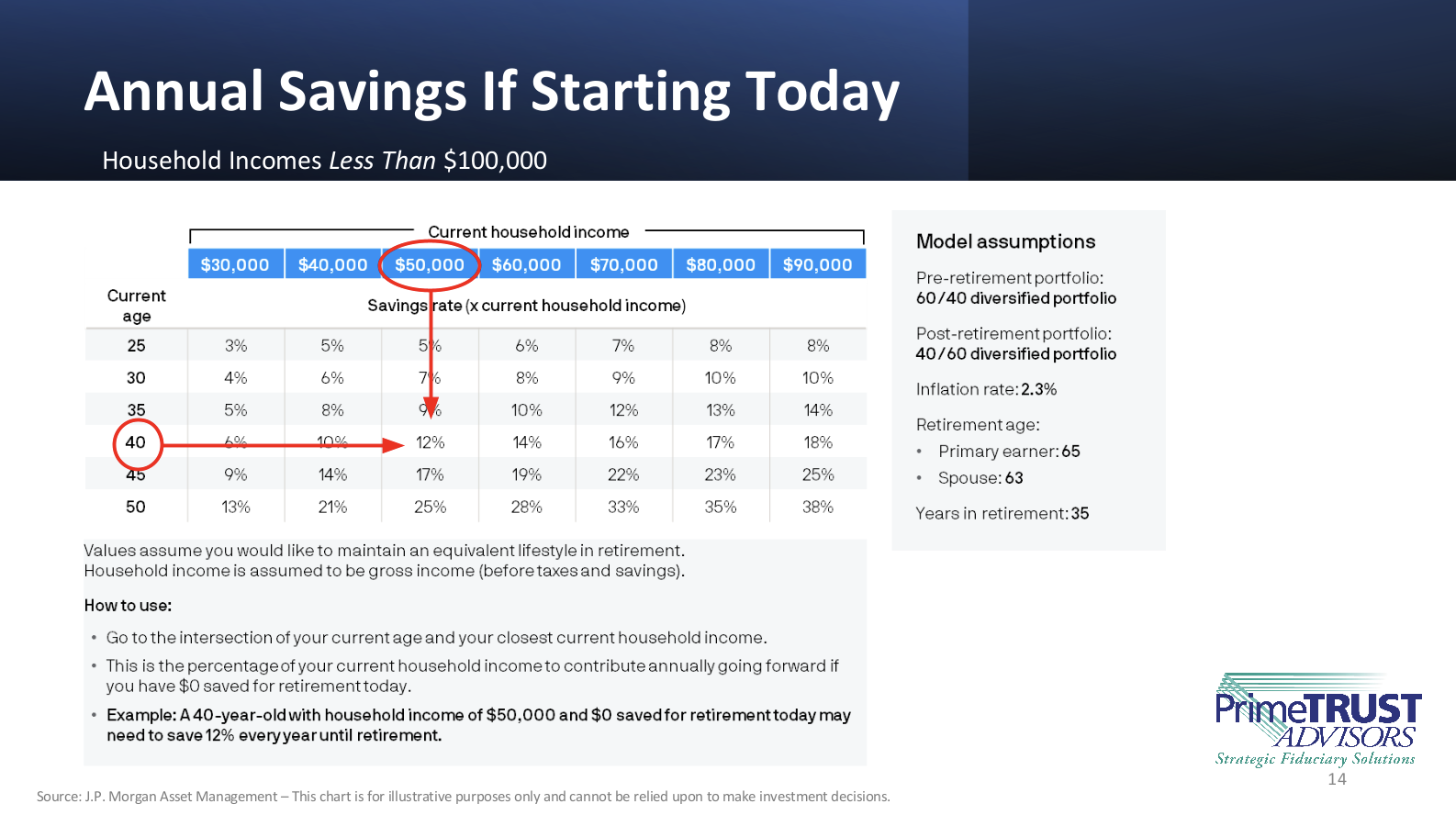

This chart assumes that someone is just beginning to save. Using a hypothetical example of a 40-year-old, let’s go to the intersection of age and household income to find the suggested savings rate. So, taking our 40-year-old making $50,000 a year, and finding the intersection of the two, you will see this individual has a suggested contribution rate of 12% each year to meet his 33% goal we mentioned above. Now we know what the goal is: provide paychecks at 33%. And we know how much it’s going to cost each year: 12%. We’ve solved the problem!

When using these charts, keep in mind:

- The income figure shown here is combined household income. So, a spouse’s income would be counted in this number, meaning that together, they’re making $50,000 (one person may be making 30,000, the other person may be making 20,000).

- Typically your employer also contributes to the plan. So those employer contributions help you get to the 12%.

Continuing with our 40-year-old, let’s assume he works for a company with a matching contribution rate of 50% of what he puts in, up to 6% of his wages. He decides, based upon all the advice he’s heard, he should max out on the company match. This means that if he puts in 6% of his pay and his employer puts in half that amount (or 3%), he’s now at 9%—which of course, is short of the 12% he needs. And that’s also the problem for so many other people. To get to the suggested contribution rate of 12%, he needs to increase his contribution another 3%. That, plus the company’s match of 3% gets him to his 12% target. Notice that with the employer’s help, it only cost him 9% to get to the 12%.

But what if this individual’s spouse works for a company that also has a 401(k) plan with the same matching contribution formula? Under these circumstances, he could put in 4% and get a company match of 2%, for a total of 6%. And if his spouse did the same thing, well, 6 plus 6 is 12. And now it only costs them 8%. It’s like money is on sale: $8 buys you $12! So, the point is that spouses should work together to figure out the most efficient way to hit their suggested contribution rate for funding their retirement paycheck goal.

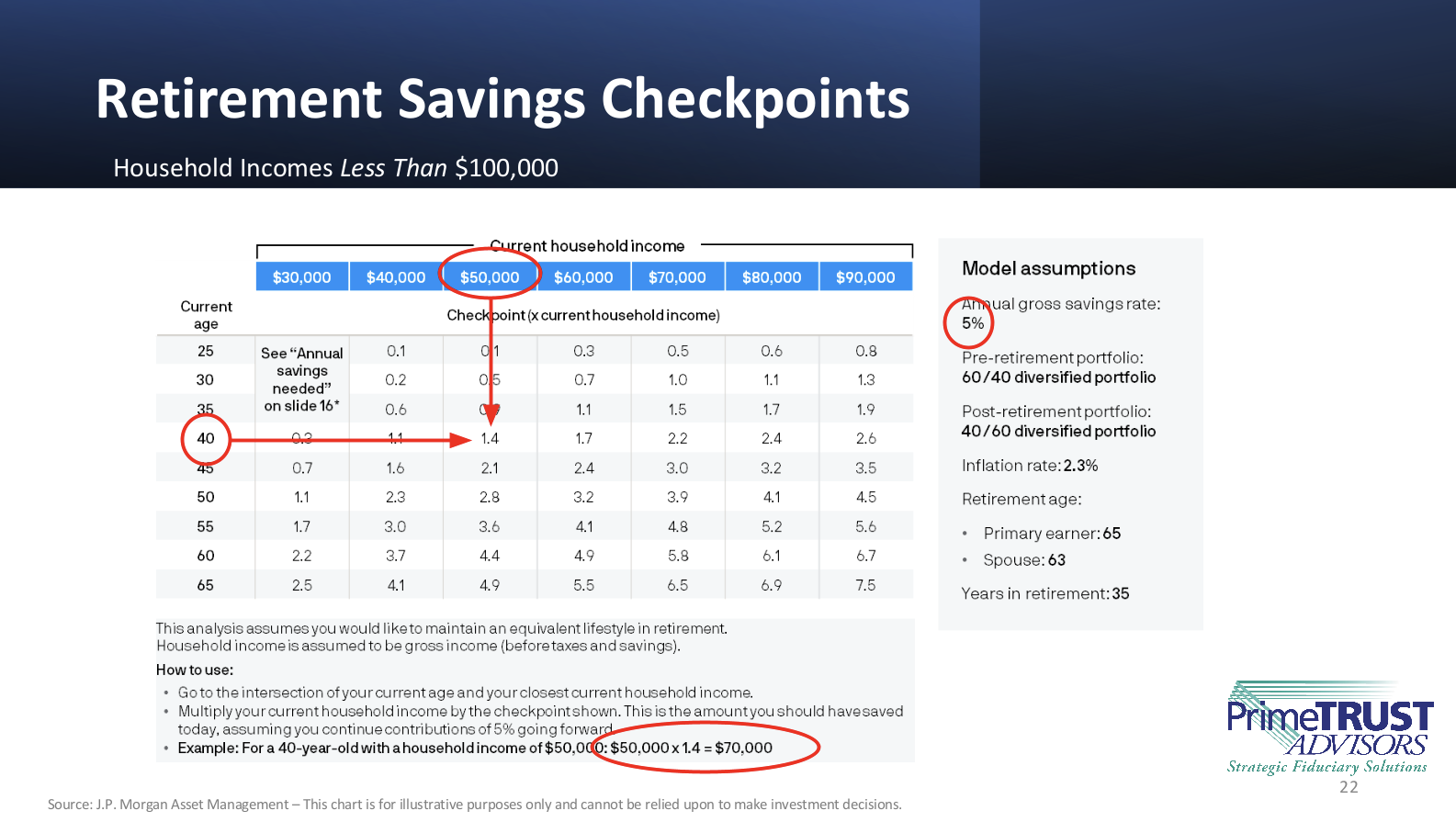

But what if this guy and his spouse have been saving all along? The chart above helps you determine how much money they should have already accumulated in their retirement account if they expect to hit that 33% paycheck goal in retirement. This amount is determined by multiplying your household income by the factor shown on this chart. This gives you a checkpoint to measure yourself by to see if you’re on track. (Again, this chart is for those households bringing in combined incomes of less than $100,000.)

With our hypothetical 40-year-old, you can see that his multiple is 1.4 times his household income of $50,000, which equals $70,000 as the amount of money he should have already accumulated in his 401(k) plan. That, and continuing contributions of 5% a year to the plan, should get him on track to meet his goal.

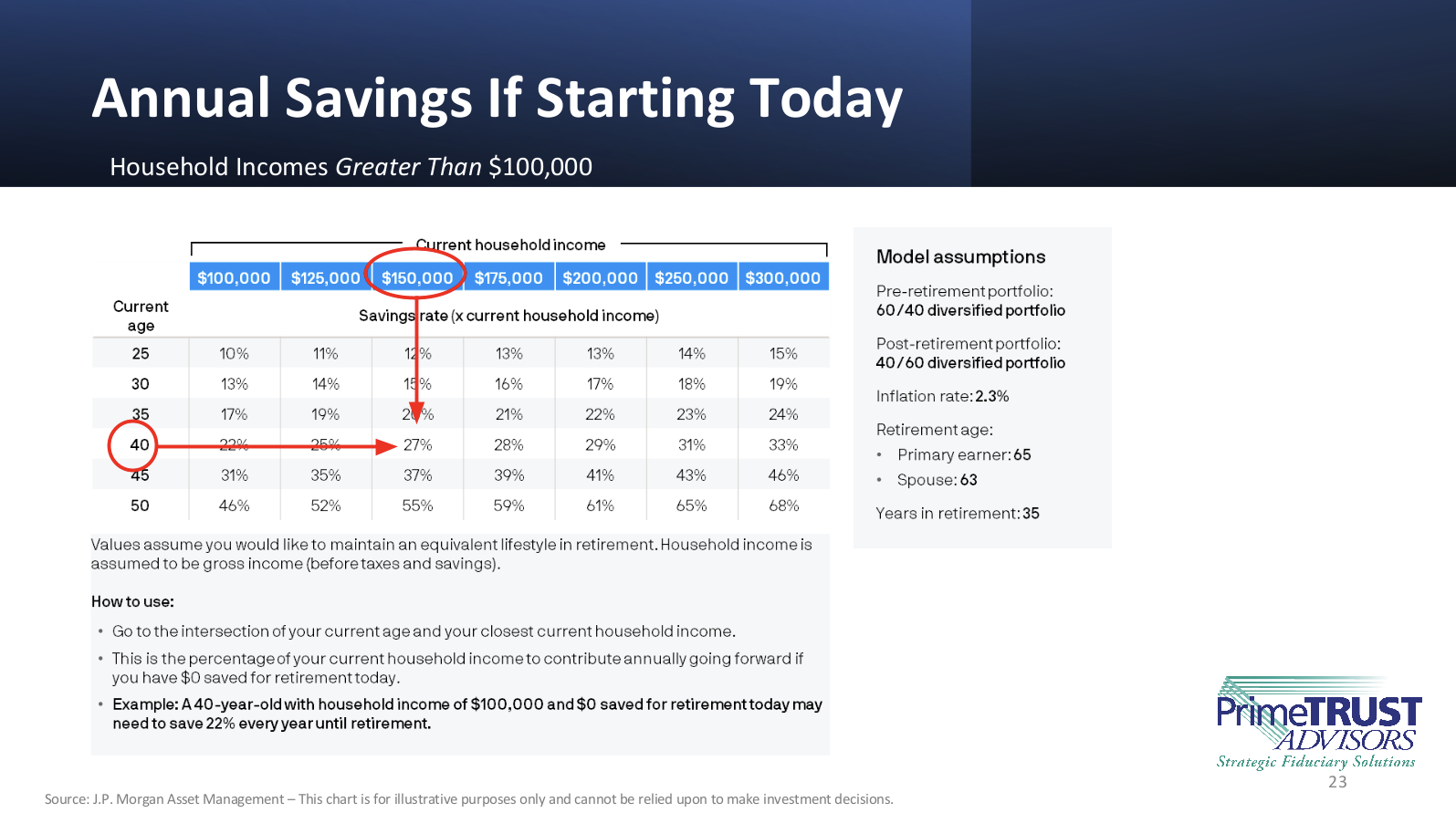

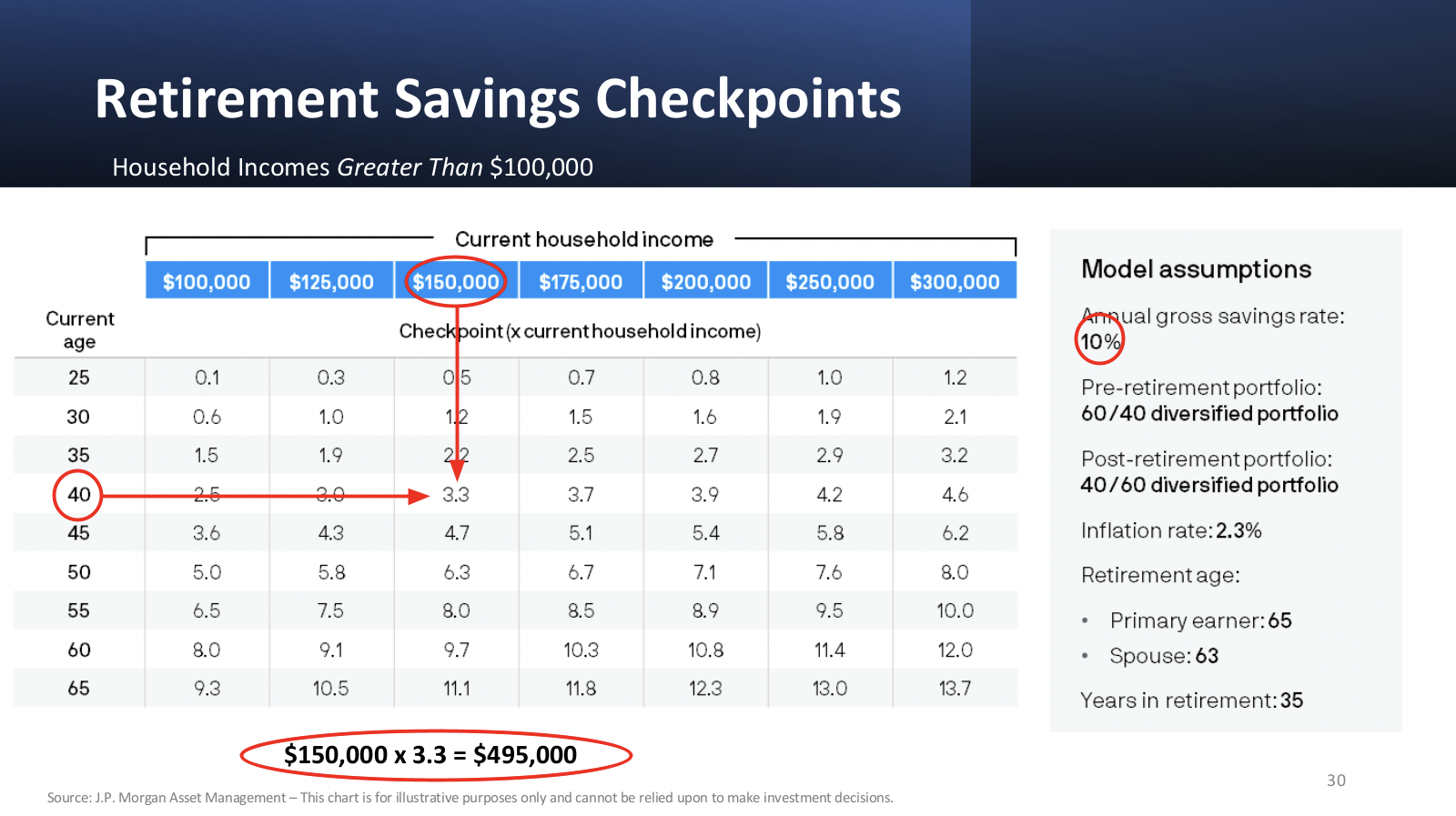

Now looking at the guidelines for those households making more than $100,000, in this case, we can see that a 40-year-old is making $150,000 a year. If just starting out today, significant contributions will be required to hit his goal. That, of course, is more than double the 12% rate we were just looking at.

Why do you think that is if they’re both the same age? You may recall from the first example, the retirement goal (in blue) was to provide regular paychecks of only 33% because Social Security provided 61%. For someone making $150,000, you will notice Social Security provides only 33%, meaning that the goal in this case is to create a paycheck of 47% of what they were making before retirement. That’s their goal, which is significantly larger than the 33% in the prior example. So that’s how we came up with the suggested contribution rate of 27% in this case, compared to the 12% discussed previously.

Now let’s look at the retirement savings checkpoint. (Remember, this chart shows how much money someone should have already accumulated in the retirement account.) Like before, this is expressed as a multiple of household income. You’ll see that this multiple is 3.3%, more than twice the multiple of 1.4 in our earlier example. Doing the math, $150,000 times 3.3 gives you $495,000 as the amount that should be in their account today. Notice that they also need to be contributing 10% of their combined household income to hit their retirement paycheck goal. Again, as mentioned before, the couple needs to work together to determine the most efficient way to do that.

As we said in the beginning, you as the chief decision-maker carry the responsibility for making your 401(k) work. Following these guidelines can go a long way to helping you fulfill that responsibility by setting your sights in the correct contribution rate. Don’t shortchange yourself on your retirement.

We’re Here to Help

We hope we’ve been able to give you some basic insights on how to think about setting your retirement goal and helping you with the math for deciding how much to contribute.

If you feel like you might be behind and could use some sound coaching from a pension guy on how to catch up, don’t be shy! You’re not alone; many people are struggling with this. Our PrimeTRUST Advisors team is here to help.

If you have questions or would like some more information, please get in touch with us today! We’d love to hear from you and make sure you know about our next upcoming tutorial on 401(k)s: How to Invest.

About Chip

Chip Hunt is the founder and President of PrimeTRUST Advisors, an investment advisory firm dedicated to helping individuals and institutions with their retirement plan. His desire to embrace the true fiduciary role (working for the best interest of others) motivated him to launch the firm in 2006 to transform this belief into a reality.

Chip graduated from the University of the South (Sewanee, TN) with a BA in English. He credits his “formal” education to his 40 years in the financial services industry, most of which were spent growing up as the 3rd generation in his family’s actuarial services firm managing corporate pensions, 401(k)s, and designing investment structures within those plans. Chip serves in leadership roles in retirement industry organizations and is an author and frequent speaker on retirement topics. Mostly though, Chip loves working “in the trenches” alongside his clients, seeking to serve their needs in this specialty field.

Chip loves the outdoors! He’s been known to sneak out of the office “due to weather conditions” and hit the Swamp Rabbit Trail on his bike. Either that, or you’re likely to find him on a near-by hiking trail.

Fun Fact: At Sewanee, Chip served 4 years on the student-led, community fire department as the chief-engineer (the driver of the firetruck).

To learn more about Chip, connect with him on LinkedIn.