Posted by PrimeTrust Advisors | January 22, 2023

High Interest Rates Present New Opportunities for Taking Your Pension

By Chip Hunt

“High interest rates are changing the math on pension lump sums.” – The Wall Street Journal, October 31, 2022

The Punch Line

So…here’s the punchline!

Because of the way pension rules work, changing interest rates often create pricing “irregularities” that you can exploit…potentially resulting in a higher pension payout to you!

And as everyone knows, we are in a changing interest rate environment RIGHT NOW. Here we discuss how you can spot pricing irregularities and steps you can take to capture the opportunity. But first, let us explain what the heck it is that we are talking about.

Your Opportunity

Many employers still offer old-fashioned “defined benefit” pension plans. The primary feature of these plans is the monthly payment amount that it pays you for your lifetime…just like Social Security. Where this gets interesting is, many plans (but not all) offer employees the option of taking a lump-sum payout rather than the monthly payments.

Now, follow me here, while the monthly payment option from your employer’s plan is generally locked in for a specific dollar amount, the dollar-value of your lump-sum payment does vary each year. The mathematics for determining the dollar-value of the lump sum is largely a function of interest rates! Your employer can give you the current lump-sum value of your pension, so you don’t have to worry about trying to calculate it yourself.

So, What’s in it for You?

The opportunity for you lies in the fact that for most pension plans, the interest rates used to calculate the lump-sum values payable from your employer’s plan are: 1) locked in once a year and 2) set for the entire year! This rule creates the opportunity for would-be retirees to easily “shop” rates during the year to spot pricing “irregularities” that may exist in their favor.

Let’s look at the table below to see how this can work. BUT…first, let me be clear before you read below, THIS IS NOT AN ATTEMPT TO SELL YOU AN ANNUITY…I promise!

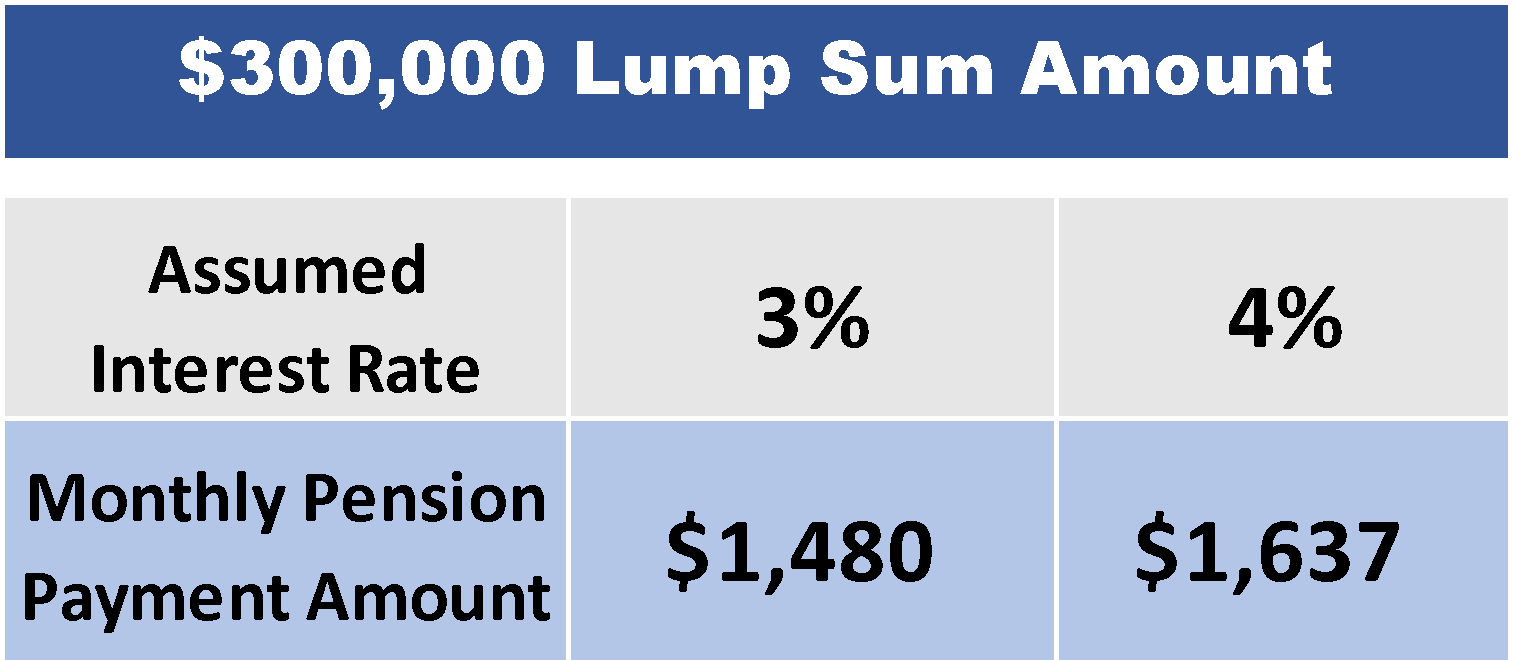

In this sample case, a $300,000 lump-sum amount is available to an employee named “Joe.” Within Joe’s employer’s pension plan, that lump-sum amount will pay Joe a monthly pension of $1,480 for life based upon an illustrative interest rate of 3% which—you will recall—is locked in at the beginning of the year.

Now, to the point above, if interest rates continue to climb in 2023, Joe should be able to buy more monthly income outside the parameters of his employer’s plan with a Single Premium Immediate Annuity (SPIA). The higher interest rates climb, the higher the amount of additional monthly income provided by a SPIA. As a general rule of thumb, for each 1% increase in interest rates, there is a corresponding 10%-12% higher monthly payment available from a SPIA depending on one’s age. In this illustration, a rate increase to 4% would provide Joe the opportunity to take the lump-sum distribution from his employer’s plan, make a direct rollover into an IRA, and purchase a SPIA to pay him $1,637 each month. That’s $1,844 more pension each year!

This idea is like shopping for more favorable mortgage rates than the one that you might be currently “stuck” with—thereby saving you money on your mortgage payment and increasing your cash flow. It’s FREE money!

For the best apples-to-apples comparison, it’s easy to shop Single Premium Immediate Annuity rates using online tools provided by either Fidelity Investments or Charles Schwab. Others are available, but these are simple to use and you don’t have to interact with an agent who will often try to sell you something “better”…like a fixed-index annuity. That’s apples and oranges…ignore that discussion for these purposes.

Remember, your sole purpose here is to do the math using online tools so you can spot pricing “irregularities” in order to capture the opportunity when it presents itself. Compare these monthly income figures to the figures offered by your pension plan to see which one provides you the most favorable results for the given lump-sum amount. If you need help, if I haven’t explained this well, or you have questions, please feel free to reach out.

To learn more on comparing lump sums and monthly pensions, check out our webinar online for FREE. Get in touch with us today!

About Chip

Chip Hunt is the founder and President of PrimeTRUST Advisors, an investment advisory firm dedicated to helping individuals and institutions with their retirement plan. His desire to embrace the true fiduciary role (working for the best interest of others) motivated him to launch the firm in 2006 to transform this belief into a reality.

Chip graduated from the University of the South (Sewanee, TN) with a BA in English. He credits his “formal” education to his 40 years in the financial services industry, most of which were spent growing up as the 3rd generation in his family’s actuarial services firm managing corporate pensions, 401(k)s, and designing investment structures within those plans. Chip serves in leadership roles in retirement industry organizations and is an author and frequent speaker on retirement topics. Mostly though, Chip loves working “in the trenches” alongside his clients, seeking to serve their needs in this specialty field.

Chip loves the outdoors! He’s been known to sneak out of the office “due to weather conditions” and hit the Swamp Rabbit Trail on his bike. Either that, or you’re likely to find him on a near-by hiking trail.

Fun Fact: At Sewanee, Chip served 4 years on the student-led, community fire department as the chief-engineer (the driver of the firetruck).

To learn more about Chip, connect with him on LinkedIn.