Posted by PrimeTrust Advisors | January 13, 2023

Now Is a Time for Reflection and Resolution—Goodbye 2022!

By Chip Hunt

A Letter to Retirees and Soon-to-Be Retirees

2022: The Year “Conventional Wisdom” Did NOT Work for Traditional Portfolios

Reflection First

What worked in 2022?

Answer: hardly anything.

It’s hard not to be discouraged, but hear me out on this. I am offering insight and hope into this matter.

If you are a retiree currently living off fixed sources of steady income—or you are soon planning to be—and you want to pass down a portion of your assets to your children and grandchildren, you are going to have to invest and spend in a more thoughtful manner. Furthermore…“you are also going to have to steel yourself to ignore most of the advice that’s been thrown your way.” (1)

Here’s my point…investing for income in retirement requires a different mindset and a different approach to investing. Most people (and their advisors) completely miss this very important point.

As in any industry, there can be a lot of sloppy thinking in the investment business. Over the years, commonly accepted investment principles have settled into a body of “conventional wisdom” that could be safely applied to MOST investors. Did you catch that? MOST… but NOT ALL investors.

Typical retirees DO NOT fall into the category of MOST investors.

Sloppiness is when we automatically resort to the safety of applying commonly accepted investment principles to ALL investors, failing to recognize the uniqueness of the person in front of us.

The strategy of allocating more heavily to bonds as one gets closer to retirement has become part of the body of “conventional wisdom.” The principles of “investment diversification” have also been welcomed into the body of conventional wisdom.

It’s most likely that conventional investment wisdom let you down in 2022.

- U.S. stocks declined 19%.

- Most other asset classes declined in value…significantly.

- “Diversification” as a risk management technique did not work.

- Investments placed into “safe” asset classes (i.e., bonds) recorded historical losses.

- For retirees basing their retirement income strategy on withdrawing a fixed percentage of assets each year, that strategy translates into reduced retirement income at a time when the cost of living is rising.

Now, this “reflection” is not intended to generate negative sentiment to manipulate you into a certain course of action…that’s a cheap trick. Rather, this is intended to get you thinking as you reflect…helping you consider a different mindset or a different point of view, which, I believe, is particularly well-suited for retirees. Our purpose is to speak to reality and offer insight for retirees—who rely upon durable and consistent sources of regular income—to evaluate their approach to investing. It does not change the reality, but considering a different mindset often leads to considering a different approach.

The chief challenge for most people is learning to unlearn the conventional ways of thinking that have become so ingrained within us during our pre-retirement years.

But to consider a different approach involves establishing absolute clarity on precisely what your financial goals are for retirement. If your goals are to establish and maintain a durable and consistent income stream to supplement Social Security and your pension (if you’re lucky enough to have one), I would suggest that you read on.

Next, Resolution

This time of year, “resolution” customarily involves making positively directed decisions to do something different going forward with the expectation of effecting better outcomes in the future.

“Resolution” can also mean devising new methods—to replace old methods—for solving old dilemmas, which is to say, “re-solving” them. (2)

You must ask yourself, “What goal am I ‘re-solving’?”

If, as stated above, your goal is to establish and maintain a durable and consistent income stream, then THE MOST important thing that matters to you—more than anything else—is the consistent delivery of an expected amount of cash deposited into your checking account month after month, year after year, for the rest of your days. That’s it…period! Remember, as a retiree, you must think differently, you are in a different category!

Your “TRUE GOAL” then becomes the delivery of an expected amount of income (cash) into your account for the rest of your life.

You are NOT interested in discussions about fancy rates of return or even bad rates of return. Those matters are irrelevant for your purposes!

Understanding your “TRUE GOAL” is gigantic progress. That knowledge helps you develop a keen understanding of what your “TRUE RISKS” are, which, in turn, is incredibly instructive for knowing how to look at your risks and how to measure it in real-world terms.

The advisory industry tends to look at portfolio risk in terms that are isolated from a retiree’s real-world mindset. Defining risk in terms of portfolio volatility does not speak to what is actually at risk for a retiree.

“TRUE RISK” for a retiree means NOT receiving deposits (income) in your checking account to meet your retirement living expenses.

Getting really clear on your goals in your real-world terms—your “TRUE GOAL” and “TRUE RISKS”—can help you reshape your vision of an investment strategy made to fit those important parameters.

A “Different” Approach for Re-Solving the Retirement Income Dilemma—“Old” Is “New” Again

For purposes of consistency in illustrating how this approach can fit within the parameters of a retiree’s TRUE GOAL and TRUE RISK objectives discussed previously, I am over-simplifying the approach to aid in communicating my principal points.

The premise of the strategy is to construct a portfolio of assets that is capable of generating lots of durable and consistent cash for depositing in your checking account.

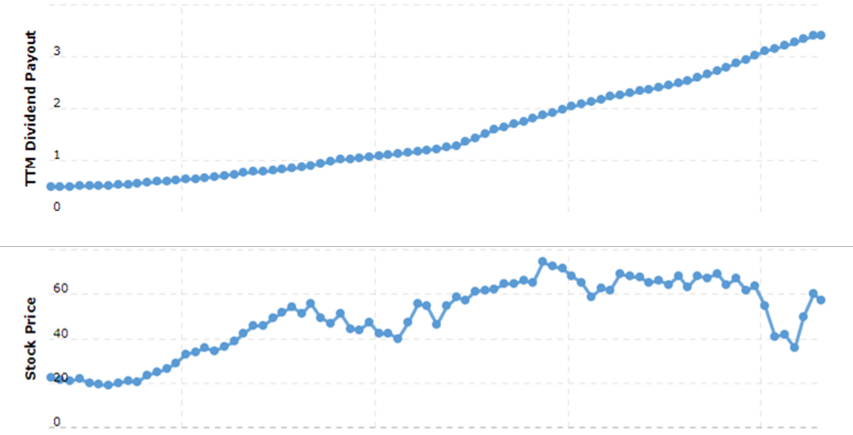

I’m a visual learner, so I’ve included the chart below that portrays the historical performance of a hypothetical income-generating portfolio to give you a structural reference to support our premise.

The top portion of the chart plots the history of dividend payouts in cash as income to investors.

The bottom portion of the chart shows the movement of the portfolio’s combined stock price over time with its typical ups and downs. This stock price portion of the graph is the part that most people follow obsessively. It’s also the portion that the media over-hypes.

A quick comparative glance at the two lines will convey an important point…the volatility of dividend cash payments DOES NOT match the volatility of stock prices. This has important implications for retiree investors seeking durable sources of income that align perfectly with a typical retiree’s TRUE GOAL and TRUE RISK parameters.

POINT #1: A Source of Income: Dividends provide a consistent source of durable income that remains fairly constant—though not perfectly stable—while also gradually increasing over time to offset the effects of inflation. Imagine each one of those blue dots in the top portion of the chart as deposits into your checking account, irrespective of the stock’s price!

POINT #2: Market Volatility Does NOT Disrupt Your Retirement Income: Stock prices (fancy returns or bad returns) are generally irrelevant to the generation of dividend income for investors. Dividends are generally a source of pride for many U.S. companies; they do not frivolously cut their dividends. In truth, there will periodically be times when dividends may be cut or paired back, but the hypothetical income-generating portfolio should maintain a “reserve” to keep the income flowing out to the retiree on such occasions.

POINT #3: Expect Your Core Portfolio to Appreciate in Value: Long-term stock prices do tend to increase in value despite wildly fluctuating market prices over the short term (consider 2008 & 2022).

POINT #4: Keep Your Core Portfolio Intact: The idea behind constructing a dividend income-generating portfolio is to produce sufficient investment “offspring” (in the form of dividends and interest from the core investment amount) to support cash deposits into your checking account without having to rely on the strategy of selling your shares for a profit to generate income to you. Keeping the number of shares consistent and the corresponding dividend payouts consistent is the secret to success, not the change in share price.

Looking Forward

I do hope that it is going to be a happier 2023 for many of you who have endured through a grueling year.

“Resolve” can also carry the meaning “to decide firmly on a course of action.”

If you wish to discuss your future course of action and how these income-generating portfolio concepts might work for you, we’d love to hear from you.

Interestingly, rising interest rates are making CDs a viable income source for generating reasonable income in retirement. Annuities, in all their various flavors, also are a source of consideration for delivering a durable and consistent income stream to your checking account. My purpose has been to give you an alternative strategy to consider. The good news is that you can combine an income-generating portfolio with other income-producing approaches. Just be aware that there are trade-offs with each strategy. Make sure you’ve been given a good explanation of those tradeoffs before you ultimately decide.

Also, if you have experiences, insights, questions, or input you would like to share, we’d love to hear from you.

You can email me at Chunt@primetrustadvisors.com or check out our website at www.PrimeTRUSTAdvisors.com.

All the best!

Chip Hunt

About Chip

Chip Hunt is the founder and President of PrimeTRUST Advisors, an investment advisory firm dedicated to helping individuals and institutions with their retirement plan. His desire to embrace the true fiduciary role (working for the best interest of others) motivated him to launch the firm in 2006 to transform this belief into a reality.

Chip graduated from the University of the South (Sewanee, TN) with a BA in English. He credits his “formal” education to his 40 years in the financial services industry, most of which were spent growing up as the 3rd generation in his family’s actuarial services firm managing corporate pensions, 401(k)s, and designing investment structures within those plans. Chip serves in leadership roles in retirement industry organizations and is an author and frequent speaker on retirement topics. Mostly though, Chip loves working “in the trenches” alongside his clients, seeking to serve their needs in this specialty field.

Chip loves the outdoors! He’s been known to sneak out of the office “due to weather conditions” and hit the Swamp Rabbit Trail on his bike. Either that, or you’re likely to find him on a near-by hiking trail.

Fun Fact: At Sewanee, Chip served 4 years on the student-led, community fire department as the chief-engineer (the driver of the firetruck). To learn more about Chip, connect with him on LinkedIn.

______________

(1) Memo to the Darcy Family: To Thine Own Self Be True, a speech by Jim Garland, June 2013

(2) Resolution and Confidence by David Kelly, Chief Global Strategist at J.P. Morgan Asset Management, January 3, 2023